Today I am talking about why your chances of getting funding without collateral (or connections) are so low that you shouldn’t even bother and why you should only start looking for money to grow a business. I need to get this out of the way because it creates a “Waiting for Godot” mindset of people walking around looking for funding for their business and sending cold emails instead of actually taking small steps to start something rather than pursuing a dream that will never be realised.

TL;DR South Africa does not have an ecosystem that supports entrepreneurs and you will end up waiting for a day that will never come.

A lot of people in South Africa go from pillar to post looking for funding for their startup dream business. Oftentimes these people are given false hope “go here or there” or “write a business plan” (bullshit! even if Warren Buffet wrote you business plan you won’t get funding). That is because people think that things in SA work like in Silicon Valley or the movies or in developed countries. It does not work like that and the worse part is that many of the startup and finance “influencers” are so in their own bubble that they tell people it does and that they should prepare pitches while leaving out very key details, which is that like anything else there is a lower end where most are, a middle and a top and if you at the lower end no matter what you do your chances of getting funding is almost zero. Now you are thinking but “I read this here and that there that they giving funding”. Well, don’t let me stop you. But let me be clear: I have never seen a startup get funding in SA based on a business plan or pitch without the stuff that a normal person at the lower end does not have (collateral, connections). All I see are people spinning their wheels looking for funding and not getting anywhere.

Now if you have been here a long time you know that I advocate starting a business with a “bird in hand” what you have available right now. I call this a “means to an end” business but even though it’s not your endgame it will help you get there. This is the only way that I know of that works on the lower end. Instead many people opt for a “dream” waiting for funding to arrive so they can start their business and it never arrives.

Further Reading

How to Fund a Business in South Africa Part 1 – Introduction

How to Fund a Business in South Africa Part 2 – Initial Funding

How to Fund a Business in South Africa Part 3 – Working Capital, Debt & Equity

We will look at the various components that make up the discussion.

As you would agree there are three main “stages” of a business (before selling or closing down):

Starting a Business

Running a Business

Growing a Business

And there are usually three main external (not friends or family) sources of finance:

Banks

Private Investors

Government (in countries where the money is not pilfered away)

Funding to start a business

In South Africa, you will not get funding for a startup from a bank without collateral because you are too high risk (you might qualify for a personal loan if you have a permanent job). You will maybe have a 0.01% chance of getting funding from a private investor (outside friends and family) without connections. As for government, I won’t even go there. Buy a lottery ticket; the odds are about the same.

Government Finance

In well-functioning countries the main funder of seed funding for startups are usually government funds (taxpayer money), this is due to the high-risk nature, it makes sense as a government you helping your citizens pursue their dreams and if the business succeeds it will pay taxes and will employ people who pay taxes. So not only does the unemployment rate go down which makes the politicians running the country look good but they are making more money to fund more entrepreneurs. And many countries have various different funds, so if you looking for a million, you can get 200k from the Queens Trust, and 400k from the Prince’s Trust and 300k from your city trust and 100k from a small business trust etc. As you can tell from South Africa’s dismal performance in entrepreneurship and one of the (if not the highest) official unemployment rates in the world we don’t do that here. Many say the government is stealing the money, which is probably true but I am also of the opinion that most of the money is going to pay the staff of these “small business departments” and very little money is actually dispersed to entrepreneurs who is not in the inner circle of the ANC.

How banks work

Banks do not lend to startups in SA without collateral full stop. In fact in business in general there are rarely bank loans without collateral, regardless of your net worth. Even Christo Wiese needed collateral to get funding despite his net worth, if you recall his creditors forced him a few years ago to sell shares he had put of as collateral after the Steinhoff collapse. In startups you would usually have to put up something you own as collateral like a plot or property (or certain policies), as the business grows and has a track record the business (as a seperate legal entity) will quality for (secured finance) and this will often involve notarial bonds (the stuff you buy with the money will be secured). A notarial bond works like vehicle or home finance but on anything like equipment.

If you don’t want to believe me, this FAQ from Guesthouse Sale sums it up (this is normal pre-pandemic):

Should I check with a bank before I look for a hospitality property?

If you are looking for funding then yes, this would be a wise decision to make. There area a whole bunch of reasons why you should first talk to your bank to get pre-approved. One of the main reasons are that the banks will generally not give any funding for any hospitality property. The only way that the banks will consider any funding is if a potential client applies for a bond as a regular home loan and you would then have to qualify from another income that you have for the bond. You have to be sure that you are able to afford the monthly repayments. There are low occupancy months where guesthouses do not make sufficient income to cover all the costs.

What the bold is saying is, even if a guesthouse is generating income as a business, you will not get a loan by putting up the guesthouse property as collateral even if the income is enough to cover the bond. You need an external source of income and usually at least a third of that must be enough to cover the bond. That is how bad it is.

I have had personal experience of how tight banks have become. Unless a personal loan/mortgage bond is not covered at least 10 times by assets, they don’t seem interested. Or is it my imagination? Would be interested to hear what is happening out there.

— Magnus Heystek (@MagnusHeystek) May 3, 2021

Private Investors

Private investors usually invest either debt or equity into a business, in the latter they will buy a percentage (share) of the business in exchange for a sum of money. Now what many people in South Africa cannot seem to grasp is that you have different levels and at the bottom level of business, small business. There is almost no private investment activity. For the simple fact that there is almost no money to be made. Stuff like micro finance don’t work in SA, because the cost of living is too much.

Businesses have such a high failure rate on the lower end that there is almost no activity here it is just to risky. The risk/reward ratio is against the investor.

For an investor to make money, there will always be some failures, however, to compensate for this there have to be one or two massive successes out of say ten. This is not Silicon Valley, this is the ANC’s South Africa. And here success is staying alive. Most small businesses only make enough for the owner/operator there is little profit for investors.

I for one have experience in investing in the lower end, let me tell you how I operated. I used the Entrepreneur – Manager – Technician model. In this you invest in someone who has experience in an industry who wants to go on their own, maybe they weren’t making enough or maybe they got retrenched, etc. They understand the industry and business and as an investor/entrepreneur I bring money and strategy and they must execute. In general I only worked with people I know or via referrals (someone I trust vouched for a person) and even this is tough to pull off. I am moving away from funding single entrepreneurs and will instead be focussing on building infrastructure that can be used by many entrepreneurs such as shared workplaces and marketplaces. Funding single entrepreneurs makes little impact and is not very profitable, in fact as an investor you can probably just put your money in Berkshire Hathaway, unless you want to help.

So you wanting funding to enter an industry you have no experience in I don’t know one person who would invest in that.

Remember I said 0.01% chance, if you have tacit knowledge then you might get funding via investor contacts because people might seek you out. However, most people with tacit knowledge have well-paying jobs and very few want to leave. Another way you might get private investors in is if you working at a business and you hear the owner wants to sell, maybe he wants to retire or emigrate and there is potential. Then you can look at a management buyout. There are investors that do that but the company must be well established or have a sum-of-parts valuation that makes it attractive in an industry with growth potential.

Private Investors with connections

You have people that can vouch for you, this would indicate that you are very competent you might get funding.

Funding to run a business | Should you even use it?

Next, we look at working capital, this is you have already started the business, you have some traction cashflow etc., it is running and you need money for day-to-day operations just to keep things moving. Now in South Africa, there has been a slew of new players using the Wonga efficiency business model in this arena. Lulalend, Business Fuel etc. These guys give out unsecured loans (or “cash advances” to use their parlance) if you have a certain revenue turnover (according to them you are selling your future sales at a discount).

I have a big problem with these guys as they have extremely high interest rates and I don’t advise using them unless you are desperate, for example your truck or equipment broke down and you need it fixed to run your business. These guys must be seen for what they are: the payday lenders of the small business world. You cannot become dependant on these guys, go and look up people who become dependant on payday lenders, eventually all your money is being spent on loans and you have to take out another loan to pay of an old loan, it can become a vicious circle. Instruments like “re-advances” are very dangerous because you have high interest “advances” on high interest “advances”. Some of them will say it’s not a loan or an “interest-based product” but an “advance” that is just semantics. If You are lending R100k and have to pay back R140k you can call that R40k whatever the hell you like. It is interest on the money you were lent…err sorry “advanced”.

These guys must be used as a last resort as they could be detrimental to your business.

The whole South African ecosystem is a difficult place to do business and this is part of that. That being said with the way things are, the bar is so low that we should be grateful for anyone offering an unsecured loan helping hand. But the interest rates that these people charge it is roughly double what a business will pay for finance.

A well-established large business can get secured finance at <10%

A small to medium business can get secured finance at 10-20%

These guys charge as high as 40% – higher than most of our profit margins

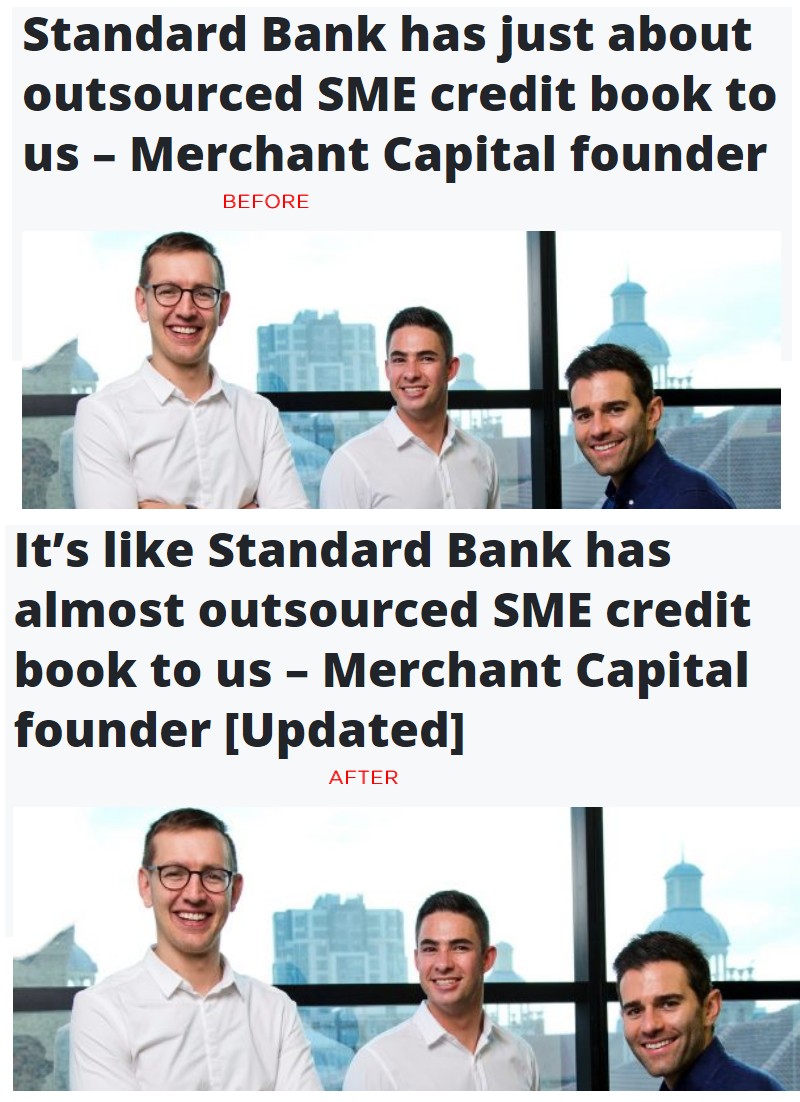

What is most distressing is that one of these companies, let slip that Standard Bank is going to outsource their small business loan book to them, in other words, banks themselves don’t even want to deal with working capital anymore, look here:

Nobody will make such a statement without some sort of agreement with Standard Bank. It is not something you make up on your own.

Nobody will make such a statement without some sort of agreement with Standard Bank. It is not something you make up on your own.

Now you thinking but banks were shit in dealing with small business and they took long at least these guys are fast and efficient. Exactly! That is part of the bad ecosystem that we have. The point I’m making is start, run and then look for funding to grow, that is the best time to access finance and even then you should ask yourself do you really need it. In business finance, you need to make sure your potential profits far exceed the interest you will be paying because like personal finance it could end up being a big problem if you lose a major source of income as creditors will force liquidation and you will lose your business (and source of income to live on). Whereas if you were not externally funded you can cushion a blow with time as there are no wolves at the door.

Bottom line: if you hoping to raise funding for your perfect dream business it will remain just that, hopes and dreams but if you are willing to work towards starting with what you have you may have a chance.

Further Reading

How to Fund a Business in South Africa Part 1 – Introduction

How to Fund a Business in South Africa Part 2 – Initial Funding

How to Fund a Business in South Africa Part 3 – Working Capital, Debt & Equity

Image credit: cartoonist